A recent reading of Howard Marks’ “Mastering the Market Cycle,” provided some valuable financial planning and investment management insights. Marks details how cycles are a permanent fixture in markets and economies, and that the cyclically-informed investor has advantages over the uninformed one. The average investor typically ends up on the wrong end of economic and market cycles. I think it would be useful to contrast a hypothetical average investor (Investor A) and his behavior over past cycles, with a hypothetical client advised by a competent advisor (Investor B). I will refer to 2 charts. The first highlights consumer confidence, the consumer savings rate, and contrasts it against the S&P 500 and consumer spending.

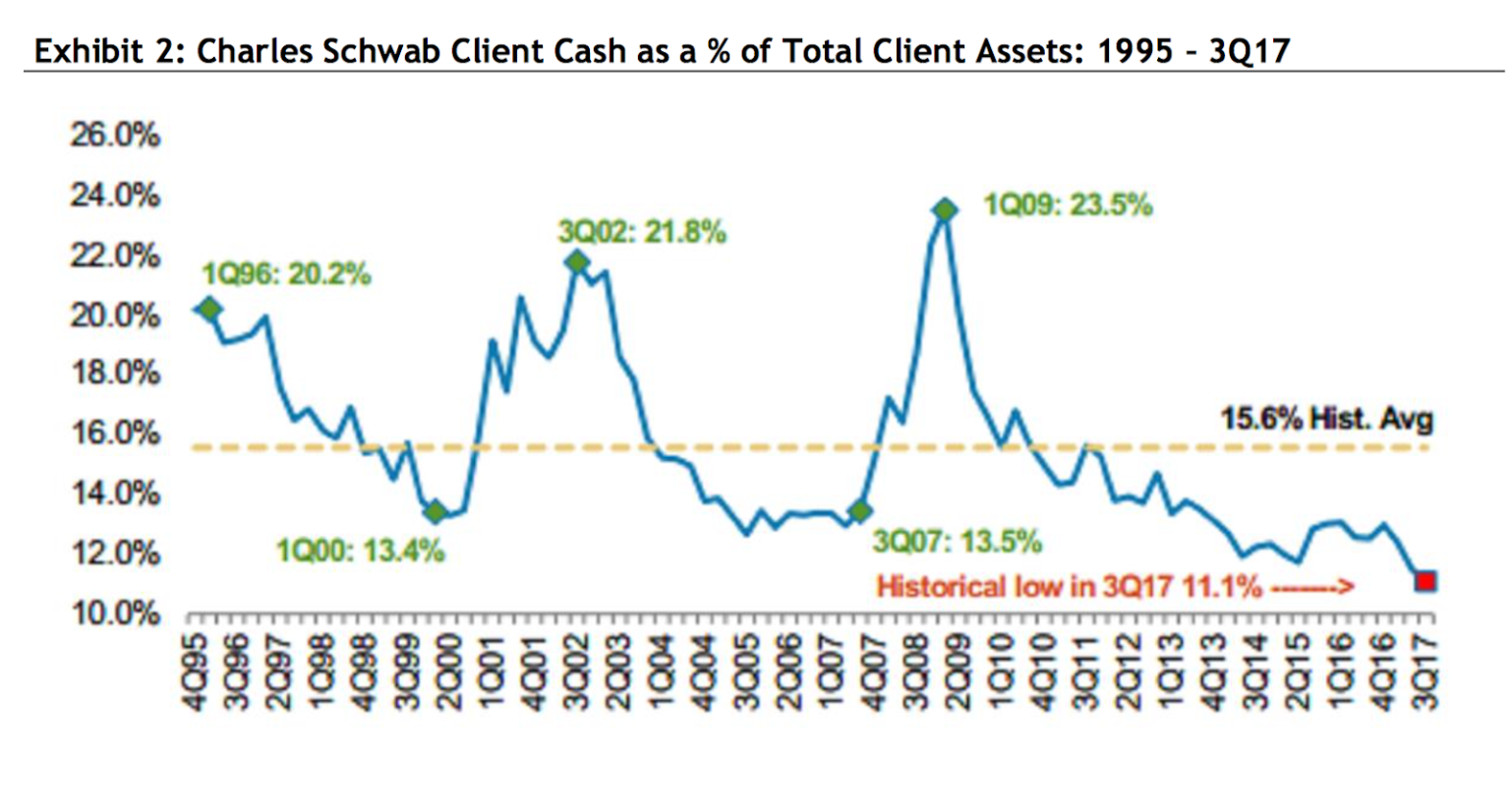

The second shows client cash levels over time at a large brokerage. By deduction, high cash signals low equity exposure and high risk aversion, with low cash implying high equity exposure and risk seeking.

Investor A’s behaviors mimics the average investor’s behavior as expressed in these charts. Investor B represents a client working with a cyclically-minded advisory firm.

Both charts begin in the early to mid 1990s. The economy was beginning to gain traction after the recession of 1991, and yet Investor A, with a tendency to look in the rearview mirror, remained cautious and risk averse. He was unconfident about the economy and markets and his personal financial prospects. He spent less and saved more. He also had low equity exposure and high cash in his portfolio. Investor B also felt unconfident in the economy and and markets. However, his advisor pointed out that the recession had created compelling valuations in housing and stocks. The economy was emerging from recession, investor sentiment was negative, and asset prices were compelling. A tilt to higher equity exposure and a more constructive view on the economy was warranted, without the need of a crystal ball.

As the 1990s progressed, and the economy and markets surged, Investor A became more confident. The economic news was positive, and his income was increasing. He spent more and saved less. Feeling the drag of low equity exposure in a surging market, he began to rapidly increase exposure. The higher the market went the more confident he became. By the late 1990s investor A’s balance sheet had degraded as he continued to saved less and less. His rationale: “Why save money when your house and investment portfolio are surging?”

Investor B, after adding stock exposure in the mid 1990s, saw his portfolio show large returns. Nevertheless, he felt the emotional pull to add even more exposure, and felt he was missing out on surging tech stocks. His advisor explained that the economic and market cycle were very mature, investor sentiment had become worryingly bullish, and valuations-particularly in tech stocks-were very high. While not predicting a market crash or recession, he advised increasing caution. He recommended a move to build balance sheet liquidity, increase savings, accelerating debt paydown, and a reduction in equity exposure.

The resulting recession and bear market in 2000-2002 badly impaired Investor A. His heavy equity allocation resulted in a very large drop in his portfolio. This was made worse by a sharp deterioration in his balance sheet. He had been spending heavily due to his surging home equity and portfolio. Now both were down considerably, and his overleveraged and illiquid balance sheet was adding to the stress. By 2002, all the economic and financial news was bad, and the market and his portfolio seemed to have no bottom. Finally, overcome by fear and anxiety, he dumped a large portion of his equity portfolio.

Investor B was not unaffected. The value of his home had fallen. His portfolio, while down, was down considerably less than the market. He also read the news, and felt anxiety and pessimism. HIs advisor explained that the recession would not continue forever, that equity valuations had dropped to compelling levels, and widespread investor fear and pessimism were a positive signs for future returns. He suggested shifting a portion of the investor’s liquidity into his portfolio, and to slowly increase equity exposure.

This simple hypothetical example serves to highlight the impact of cycles on different investors. The average investor continues to fall into a recurring pattern of making the same mistakes, typically to the detriment of his financial health. This is due primarily to a combination of procyclical behaviors coupled with the inability to control emotions. This is not an intelligence issue. In my experience, smart, driven, time-constrained professionals often are just as susceptible to making the same mistakes. For this reason, working with an advisor who frames the economic and market cycle for his clients, and calibrates his client’s behavior and emotions based on the current position in those cycles, can often help his client experience far better financial and investment outcomes over the long-term.

ryanpdolan@dolanpartners.com